The PLAC III project has provided support to the Tax Administration of Serbia in introducing with the latest EU rules in the area of prevention of tax frauds/misuses committed by shell companies and providing recommendations for harmonisation of the legislation with Union acquis.

EU member states are faced with the appearance of entities that operate as shell entities, therefore, distinguishing between business entities with real commercial operations from legal entities with no minimal substance and economic activity for purposes of fair enforcement of tax law becomes challenging. The European Union has made several efforts to impose stricter rules on the use of shell companies. In December 2021, the European Commission presented a directive on preventing shell companies from misusing their structure for tax purposes and amending Directive 2011/16/EU on administrative cooperation in the field of taxation. That proposal was adopted by the European Parliament in January 2023 and is now in the further procedure.

The proposal introduces a 'filtering' system for EU company entities, which will have to pass a series of gateways related to income, staff and premises, to ensure there is sufficient 'substance' to the entity. Those entities that are deemed to be lacking in substance are presumed to be 'shell companies' and, if they are unable to rebut this presumption through additional evidence regarding the commercial, non-tax rationale of the entity, they will lose any tax advantages granted through bilateral tax treaties or EU directives.

The Serbian Tax Administration is the competent authority within the Ministry of Finance in charge of the assessment, audit and collection of public revenues and suppressing any form of tax evasion. The Tax Police, as a separate sector in the Administration, is authorised to detect tax crimes and their perpetrators.

The support of the PLAC III project included the assessment of legal gaps in relation to the EU rules applicable to the fight against tax evasion through shell companies, providing recommendations for improving the legal framework for combating the misuse of shell companies for tax avoidance and establish appropriate criteria and tools for the early detection of shell entities based on best practices of EU member states.

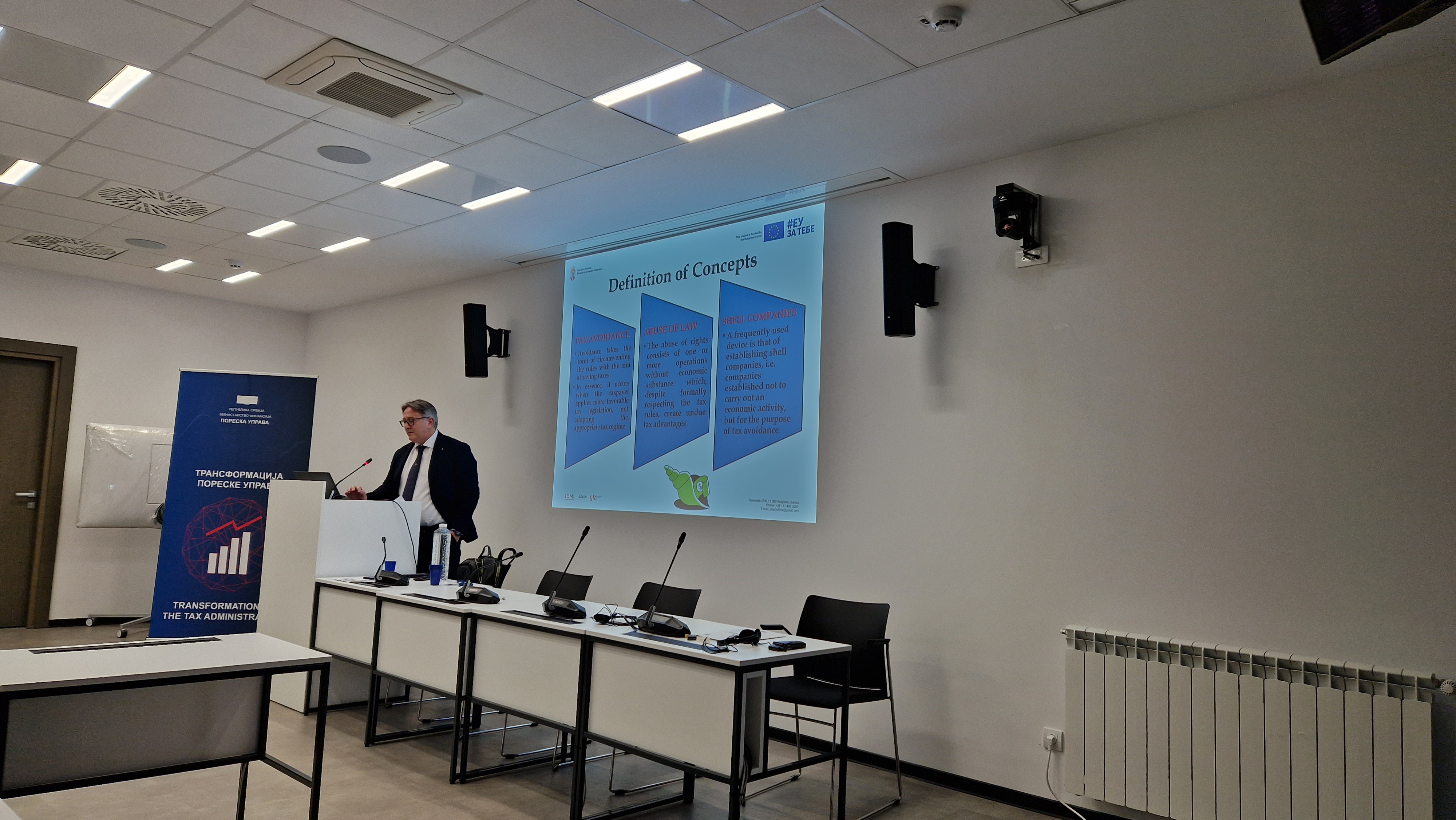

On 1 February 2024, at a workshop held in Belgrade, project expert Giacinto Capone presented the provisions of the EU Council Proposal for a directive establishing rules for preventing the misuse of shell companies. One of the main purposes of its enactment was to enable the identification of shell companies established solely for tax purposes, Capone said. He gave the overview of the criteria for determining the suspicion that it is about a shell company, what are the indicators for that, as well as which prevention measures are envisaged.

Capone then presented the results of the analysis of legal gaps in Serbian legislation against EU legislation. He said that the Republic of Serbia, even though it is not a member of the European Union, in the period of accession should harmonise its national legislation with Union acquis, while it would postpone the application of certain provisions of the same law until the moment of accession to the EU.

The Law on Tax Procedure and Tax Administration does not contain a definition of shell companies. Among Capone's recommendations, he stated that the concept of minimum economic substance should be defined, the method of filtering shell companies should be envisaged, as well as two tests and their criteria: the entrance test and the minimum economic substance test. Also, it is necessary that the Law provides the possibility of automatic exchange of data between the national tax authorities of different countries at the level of the European Union.

The workshop was held for representatives of the Tax Administration and the Ministry of Finance.